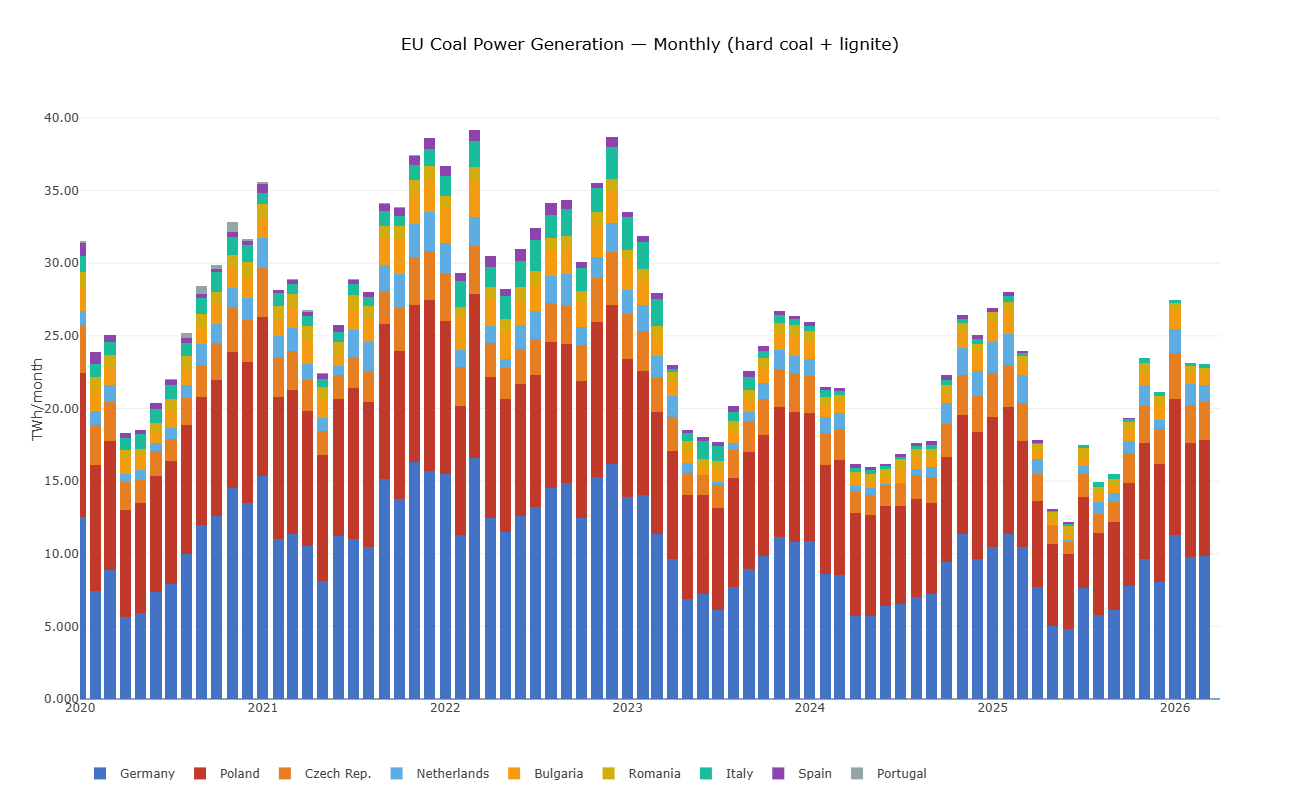

The aggregate numbers are real — EU coal generation fell from ~417 TWh in 2022 to ~242 TWh in 2025, a 42% drop in three years. But the country-level data tells two completely different stories — one western, one eastern.

I built out coal generation tracking across 16 European countries using ENTSO-E actual generation data, hourly resolution from 2020.

The western exit is essentially complete

Portugal closed its last coal plant in 2022. Spain went from 10.6 TWh in 2019 to 1.3 TWh in 2025. Italy: 17 TWh to 2.7 TWh. France was already marginal — a few TWh in stress conditions, structurally irrelevant.

Germany is the one everyone watches, and the decline is real: from a 2022 gas-crisis peak of 166 TWh down to 95 TWh in 2025, a 43% drop. The lignite fleet is still running, but the direction is unambiguous.

The 2022 spike — when the gas crisis forced coal back into the dispatch order across the whole continent — now looks like what it was: a last gasp. The recovery to pre-crisis renewable trajectories has been faster than the 2022 commentary suggested.

Then look east

Poland generated 83 TWh of coal power in 2025. That is, for context, nearly as much as Germany — a country four times the size of Poland's economy. Poland's decline is real (down 32% from its 2021 peak), but at this pace it will still be generating 50–60 TWh of coal well into the 2030s.

Czech Republic is flat at 23.7 TWh in both 2024 and 2025. No declining trend at all. CZ has no firm coal exit date and the numbers reflect that directly.

Bulgaria has the sharpest swing: a 59% surge in 2022 (Maritsa lignite running flat out during the gas crisis), then a collapse back to ~10 TWh. The plants are aging but they're not going anywhere fast.

Romania is on a slow, steady glide path downward — from 9.6 TWh in 2020 to 6.6 TWh in 2025. No acceleration in sight.

Two markets, one market

What the aggregate EU statistics hide is that roughly 35% of remaining EU coal generation is in one country — Poland — which is almost invisible in western European policy discussions. When EU institutions report declining coal figures, they're averaging together a near-complete western exit with a structurally entrenched eastern fleet.

The implications are direct for anyone modeling EU power markets, carbon intensity, or energy security risk. The generation-weighted carbon intensity of the eastern grid is materially higher than the west, and will remain so for longer than the headline trend implies.

The 2022 gas crisis reinforced this divergence. In the west, it briefly slowed an exit that was already market-driven. In the east, it strengthened the energy security argument for keeping coal capacity available — and those arguments don't disappear when gas prices normalize.

A note on the data

All figures are from ENTSO-E actual generation data, covering AT, BG, CZ, DE, DK, ES, FI, FR, GR, HU, IT, NL, PL, PT, RO and GB — approximately 85–90% of total EU coal generation. Hard coal and lignite are combined per country.

The analysis was built with the Timeseries Refinery by Pythonian, which handles the hourly series management, resampling, and visualization across all 16 countries in a unified pipeline. The chart above is a live dashboard figure that updates automatically as new ENTSO-E data arrives.

About this analysis

The metrics in this article were built and computed using the Timeseries Refinery by Pythonian, a time series data management and analytics platform designed for energy market analysts.

The platform allows analysts to combine heterogeneous data sources (ENTSO-E and others) in a single environment, express complex metrics as simple versioned formula queries, and update results automatically as live market data arrives — without rebuilding pipelines.

Data sources: ENTSO-E actual generation.

Request a demo